Introduction : Pourquoi 2026 est un tournant pour l'emballage alimentaire jetable

Résumé rapide : Mise à jour de la politique mondiale en matière de vaisselle en plastique pour 2026

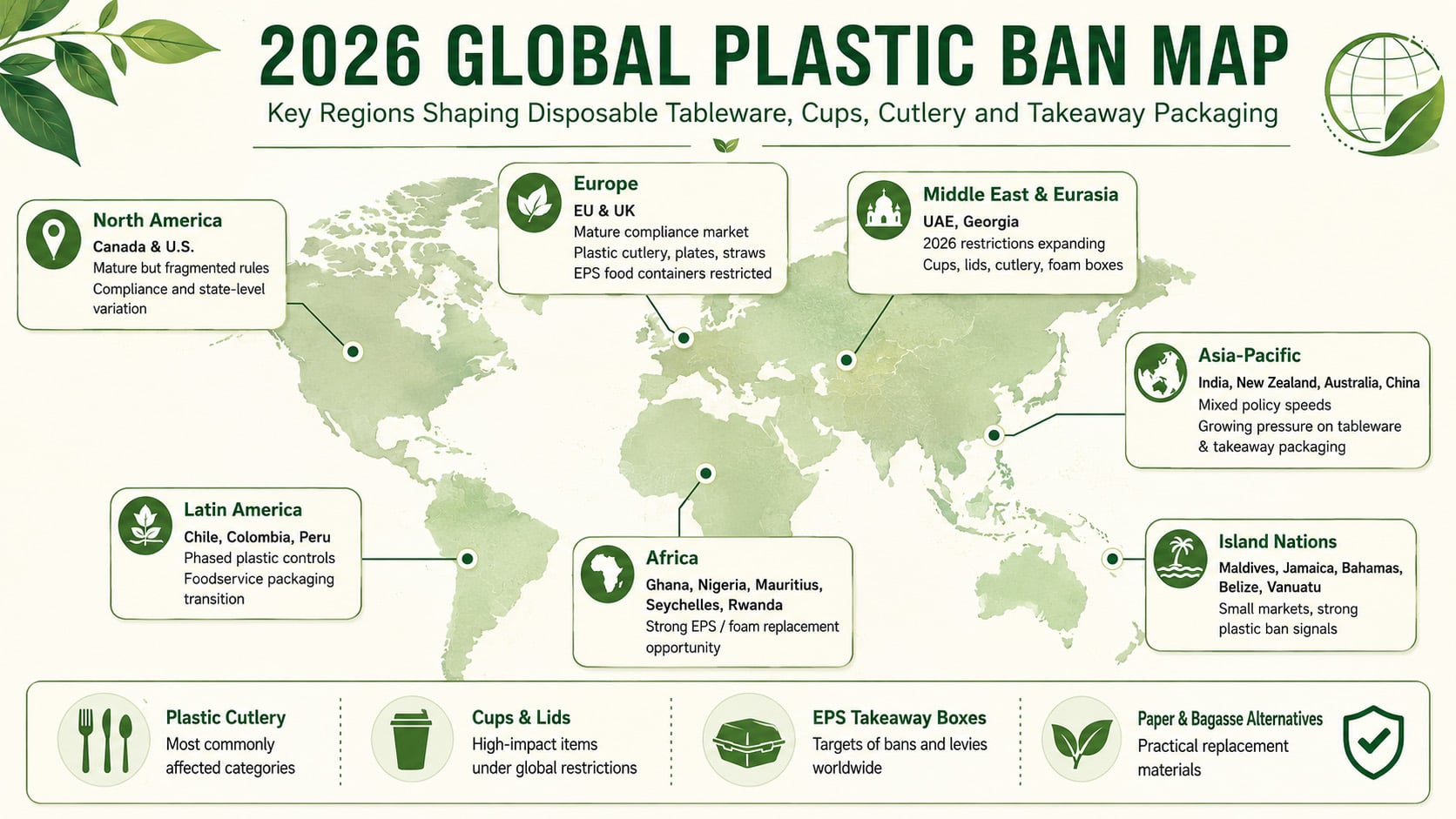

- Les emballages jetables des services alimentaires deviennent une catégorie prioritaire de la politique mondiale en matière de plastique.

- Les couverts en plastique, les assiettes en plastique, les gobelets en plastique, les pailles, les agitateurs et les récipients alimentaires en mousse de polystyrène expansé figurent parmi les articles les plus fréquemment soumis à des restrictions.

- L'Europe et le Canada sont des marchés matures en matière de conformité, où la documentation et les allégations relatives à l'emballage sont examinées de près.

- La Géorgie et les Émirats arabes unis sont des exemples importants de nouvelles restrictions affectant les plastiques destinés à la restauration.

- L'opportunité la plus concrète pour l'Afrique est le remplacement des boîtes à emporter en PSE/styrofoam, en particulier dans des pays tels que le Ghana, les Seychelles, l'île Maurice, le Rwanda et le Nigeria.

- La région Asie-Pacifique est très diversifiée : L'Inde et la Nouvelle-Zélande appliquent des restrictions plus strictes, tandis que l'Asie du Sud-Est évolue plus graduellement grâce à une réduction progressive du plastique et à une demande induite par le tourisme.

- Pour les acheteurs internationaux, la stratégie la plus sûre est un portefeuille de matériaux mixtes : bagasse de canne à sucre, carton, papier kraft, papier couché sans plastique, couverts en bois et matériaux certifiés compostables, le cas échéant.

1. Tendance politique mondiale : De l'interdiction des sacs en plastique au contrôle des emballages des services alimentaires

Au cours de la dernière décennie, la réglementation sur les matières plastiques a évolué par étapes. De nombreux pays ont commencé par les sacs de caisse en plastique parce qu'ils étaient visibles, légers et largement répandus. L'étape suivante a visé les pailles en plastique, les agitateurs et d'autres articles de petit format ayant une faible valeur fonctionnelle mais une grande visibilité environnementale. D'ici à 2026, les politiques se concentreront sur un domaine plus important d'un point de vue commercial : les emballages jetables des services alimentaires.

Cette évolution est importante car les emballages des services alimentaires sont utilisés à grande échelle. Une seule chaîne de restaurants, un réseau de cafés, un traiteur de compagnie aérienne, une plateforme de livraison de nourriture ou un groupe hôtelier peuvent consommer chaque année des millions de gobelets, couvercles, plateaux, bols, assiettes, couverts et contenants pour les plats à emporter. Lorsque les gouvernements restreignent ces produits, les acheteurs ne peuvent pas se contenter de retirer un article d'un rayon. Ils doivent reconstruire les spécifications des emballages, tester des matériaux alternatifs, vérifier les systèmes d'élimination locaux, confirmer la sécurité du contact alimentaire et garantir un approvisionnement stable avant que les réglementations ne soient pleinement appliquées.

Quatre étapes de la réglementation mondiale sur les emballages plastiques

Étape 1 : Sacs à provisions en plastique

Les premières politiques en matière de plastique se sont souvent concentrées sur les sacs à main légers. Ces mesures ont sensibilisé le public et ont permis aux gouvernements d'acquérir de l'expérience dans la réglementation des produits à usage unique en grande quantité.

Étape 2 : Pailles, agitateurs et petits articles jetables

Les pailles en plastique et les agitateurs de boissons ont été les premiers visés parce qu'ils sont souvent inutiles, difficiles à recycler et fréquemment trouvés dans les déchets marins et les déchets de rue.

Étape 3 : Vaisselle jetable et emballages des plats à emporter

Les couverts en plastique, les assiettes en plastique, les bols en plastique, les gobelets en plastique, les coquilles en mousse EPS et les conteneurs alimentaires font aujourd'hui l'objet d'une réglementation plus agressive en raison de leur lien direct avec les restaurants, les repas à emporter et les livraisons de nourriture.

Étape 4 : Conformité totale de l'emballage

Les marchés matures passent de l'interdiction à des systèmes de conformité complets, comprenant la recyclabilité, la compostabilité, l'étiquetage, la sécurité au contact des aliments, la REP, les objectifs de réduction des emballages et le contrôle des allégations environnementales.

Pourquoi 2026 est différent des précédentes interdictions du plastique ?

Les interdictions antérieures du plastique étaient souvent simples : ne plus utiliser un sac, une paille ou une boîte en mousse spécifique. L'environnement politique de 2026 est plus technique. Les régulateurs et les acheteurs se demandent si les emballages sont réutilisables, recyclables, compostables, à base de fibres, enduits de plastique, exempts de PFAS, compostables industriellement ou adaptés à la collecte locale des déchets. Cela est particulièrement important pour les produits tels que les gobelets en papier couché, les bols en fibre moulée, les couverts en plastique compostable et les gobelets en PLA transparent.

Un produit étiqueté comme “biodégradable” n'est pas automatiquement accepté sur tous les marchés. Certains pays autorisent les matériaux plastiques certifiés compostables sous certaines conditions. D'autres classent encore le PLA, le CPLA ou d'autres articles en bioplastique dans la catégorie des plastiques à usage unique. C'est pourquoi les acheteurs internationaux doivent éviter d'adopter une stratégie axée sur un seul matériau. Une approche d'approvisionnement plus souple consiste à combiner la fibre moulée, le papier, le carton kraft, les revêtements sans plastique, le bois et les matériaux certifiés compostables en fonction de chaque marché de destination.

Bioleader® Insight : La conformité fait désormais partie de la performance des produits

Pour les acheteurs d'emballages alimentaires B2B, un contenant jetable n'est plus jugé uniquement en fonction de son prix, de sa résistance aux fuites ou de son apparence. Les performances en matière de conformité deviennent tout aussi importantes. Une solution d'emballage pratique doit répondre à quatre questions : Est-elle légalement acceptable sur le marché de destination ? Est-il sûr pour le contact direct avec les aliments ? La déclaration de fin de vie est-elle étayée par des preuves ? Le fournisseur peut-il assurer une qualité et une documentation constantes à l'échelle de l'exportation ?

Catégories de produits les plus touchées par la pression politique de 2026

| Catégorie de produits | Pourquoi il est ciblé | Alternatives courantes | Point de risque pour l'acheteur |

|---|---|---|---|

| Couverts en plastique | Utilisés une seule fois, difficiles à recycler et courants dans les déchets à emporter. | Couverts en bois, couverts CPLA, couverts en amidon de maïs, kits de couverts emballés dans du papier. | Les couverts en plastique compostable peuvent encore faire l'objet de restrictions sur certains marchés. |

| Assiettes et bols en plastique | Articles à fort volume dans la restauration, les événements, les aires de restauration et les restaurants en plein air. | Assiettes en bagasse de canne à sucre, bols en bagasse, plateaux en fibre moulée, bols en papier. | Les acheteurs doivent confirmer la résistance à la chaleur, à l'huile et aux sauces pour les applications alimentaires réelles. |

| Gobelets et couvercles en plastique | Forte consommation dans les cafés, les bars à jus, les événements et les canaux de livraison. | Gobelets en papier, gobelets en papier couché sans plastique, gobelets en PLA si acceptés, couvercles en fibre. | Les gobelets en PLA sont des produits à usage froid et peuvent ne pas être exemptés de toutes les interdictions relatives au plastique. |

| Récipients alimentaires en polystyrène expansé / polystyrène expansé | Encombrants, de faible valeur, difficiles à recycler et très visibles dans les flux de déchets. | Coquilles en bagasse, plateaux en bagasse, boîtes alimentaires en papier kraft, conteneurs en fibre moulée. | Les produits de remplacement doivent répondre aux besoins réels des plats à emporter : chaleur, huile, humidité et empilage. |

| Pailles et agitateurs en plastique | Des objets peu utiles qui deviennent souvent des déchets et des débris marins. | Pailles en papier, pailles en bagasse, agitateurs en bois, pailles CPLA, là où c'est autorisé. | Le type de boisson, le temps de trempage et l'expérience des clients doivent être testés avant l'achat en gros. |

Pour les acheteurs mondiaux, la leçon stratégique est claire : 2026 est une année de préparation. Même sur les marchés où la mise en œuvre est progressive, les marques et les distributeurs de services alimentaires évaluent déjà des solutions de remplacement. Une préparation précoce donne aux acheteurs le temps de tester les emballages avec des plats chauds, des aliments gras, des soupes, des salades, des boissons réfrigérées, des itinéraires de livraison et des conditions de stockage avant que les réglementations ou les exigences des clients ne deviennent urgentes.

Bioleader® soutient cette transition grâce à une large gamme de produits vaisselle en bagasse de canne à sucre, Les emballages alimentaires en papier et les couverts compostables sont conçus pour les acheteurs du secteur de la restauration qui ont besoin d'alternatives pratiques aux emballages en plastique et en mousse conventionnels. La stratégie produit la plus solide ne consiste pas à remplacer tous les articles en plastique par un seul matériau, mais à adapter chaque catégorie de produits au matériau le plus approprié et à la demande du marché.

2. L'Europe : Des réglementations matures et des exigences de conformité plus élevées

L'Europe est l'une des régions les plus avancées en matière de réglementation de la vaisselle en plastique. Le cadre de l'Union européenne sur les plastiques à usage unique restreint déjà une série d'articles tels que les couverts en plastique, les assiettes, les pailles, les agitateurs, les récipients alimentaires en polystyrène expansé et les gobelets en polystyrène expansé pour boissons. Le cadre plus récent sur les Règlement sur les emballages et les déchets d'emballages fait également évoluer l'Europe vers un modèle de conformité des emballages plus complet, en accordant une plus grande attention à la réduction, à la recyclabilité, à la réutilisation, à l'étiquetage et à la responsabilité des producteurs.

Cela signifie que l'Europe ne doit pas être considérée comme un simple marché d'interdiction du plastique. Il s'agit d'un marché de conformité. Les acheteurs ne se contentent pas de demander si un produit jetable est respectueux de l'environnement ; ils veulent aussi savoir s'il est étayé par des rapports d'essai, des déclarations de contact alimentaire, des certificats de compostabilité, des déclarations d'absence de PFAS et des informations précises sur les matériaux. Concrètement, un fournisseur qui comprend la documentation peut avoir plus de valeur qu'un fournisseur qui se contente d'offrir un prix unitaire bas.

Orientation de la politique européenne par marché

| Marché | Orientations politiques | Impact de l'emballage des services alimentaires | Recommandations à l'attention des acheteurs |

|---|---|---|---|

| Union européenne | Restrictions SUP et conformité plus large des emballages PPWR. | Les couverts en plastique, les assiettes, les pailles, les agitateurs, les gobelets en polystyrène expansé et les récipients alimentaires en polystyrène expansé sont les principales catégories concernées. | EN13432, conformité au contact alimentaire, preuves de recyclabilité ou de compostabilité, étiquetage des matériaux. |

| Royaume-Uni | Les restrictions concernant les plastiques à usage unique portent sur les couverts en plastique et les récipients en polystyrène pour les aliments et les boissons. | Les acheteurs se méfient des articles plastifiés et des allégations de plastique compostable. | Des déclarations claires sur les matériaux, la sécurité du contact alimentaire et des alternatives non plastiques lorsque c'est possible. |

| France | Une orientation politique forte en matière de lutte contre les déchets et d'économie circulaire. | Les opérateurs de services alimentaires sont contraints de réduire les plastiques jetables et d'améliorer la performance des emballages en fin de vie. | Des alternatives réutilisables, recyclables, compostables et à base de papier avec des preuves crédibles. |

| Allemagne | Culture de conformité stricte en matière d'emballage et attentes en matière de documentation. | Les importateurs exigent généralement des dossiers techniques, des spécifications de produits et des documents de conformité. | Tests de contact alimentaire, rapports de migration, sensibilisation à l'enregistrement des emballages et à la traçabilité. |

| Italie | Les règles relatives à la compostabilité et aux emballages des services alimentaires sont étroitement liées aux systèmes de gestion des déchets. | Les produits certifiés compostables peuvent avoir des débouchés, mais les déclarations environnementales vagues sont risquées. | Matériaux certifiés et instructions d'élimination acceptables au niveau local. |

| Espagne | La réduction du plastique et la pression fiscale sur les emballages soutiennent la demande d'alternatives. | Les acheteurs de services alimentaires évaluent le papier, les fibres moulées et les options compostables. | Emballage durable rentable avec une documentation solide. |

| Pays-Bas | L'accent est mis sur l'emballage circulaire et la réduction des plastiques jetables dans le secteur de la restauration. | Les gobelets, récipients et emballages à emporter jetables font l'objet d'un examen minutieux. | Clarté de la fin de vie, preuve de recyclabilité ou de compostabilité, et performances pratiques pour les services alimentaires. |

La vraie question de l'acheteur européen : Le produit peut-il survivre à un examen de conformité ?

En Europe, la mention “biodégradable” ne suffit pas. Un importateur professionnel peut demander la certification EN13432 pour les produits compostables, la conformité au contact alimentaire de l'UE, les tests de migration, la déclaration de conformité, les déclarations relatives aux PFAS, les fiches techniques des produits, les informations sur le revêtement, les détails du carton et les données de traçabilité. Si le produit est un gobelet en papier, l'acheteur peut demander si le revêtement est en PE, en PLA, enduit aqueux à base d'eau ou autre système de barrière. Si le produit est en fibre moulée, l'acheteur peut demander s'il est exempt de PFAS, s'il passe au micro-ondes, s'il résiste à l'huile et s'il convient aux aliments chauds.

Cela fait de l'Europe un marché solide pour les fournisseurs techniquement préparés. Par exemple, boîtes à clapet en bagasse peut être positionné comme une alternative directe aux conteneurs en mousse de polystyrène expansé et aux boîtes en plastique pour les plats à emporter, mais l'argument de vente doit aller au-delà de la durabilité. Les acheteurs ont également besoin d'informations sur la résistance aux fuites, les performances thermiques, la fermeture du couvercle, la stabilité de l'empilage, l'absence de PFAS et les documents de conformité.

Bioleader® Aperçu de la situation en Europe

Le marché européen récompense les déclarations vérifiables. Les exportateurs doivent éviter les termes vagues tels que “vert”, “éco-sûr” ou “entièrement biodégradable” sans preuve. Une formulation plus forte inclut le matériau, l'utilisation prévue, la plage de température applicable, le type de revêtement, le statut de contact alimentaire, la filière de compostabilité et les limites d'élimination.

Les meilleures alternatives pour les acheteurs européens

Vaisselle en bagasse de canne à sucre

Il convient parfaitement pour remplacer les coquilles en EPS, les assiettes en plastique, les bols jetables et les plateaux à emporter. Il s'agit d'une option solide pour les restaurants, la restauration, les repas livrés et les emballages de restauration rapide.

Contenants alimentaires en papier

Les boîtes en papier kraft, les gobelets à soupe, les saladiers et les récipients en papier pour les plats à emporter restent importants pour les services alimentaires européens. Le type de revêtement et la conformité au contact alimentaire doivent être clairement indiqués avant l'importation.

Gobelets en papier couché sans plastique

Lorsque les emballages enduits de plastique font l'objet d'un examen minutieux, les gobelets en papier enduit à base d'eau ou sans plastique peuvent renforcer le positionnement des chaînes de cafés, des événements et des services de restauration d'entreprise.

Couverts en bois et couverts certifiés compostables

Les couverts en bois sont largement acceptés en tant qu'option non plastique simple. Les couverts en CPLA et en amidon de maïs peuvent être envisagés lorsque les règles locales et les systèmes de gestion des déchets acceptent les plastiques industriels compostables.

Une stratégie européenne solide doit inclure la documentation sur les produits dès le début, et non pas après que l'acheteur l'a déjà demandée. Pour les exportateurs, cela signifie qu'ils doivent constituer un dossier de conformité pour chaque grande catégorie de produits : coquilles en bagasse, bols en papier, gobelets en papier, plateaux, assiettes et couverts. Pour les acheteurs, cela signifie qu'il faut comparer les fournisseurs non seulement en fonction du prix, mais aussi en fonction de l'état de préparation de la documentation, de la cohérence des produits et de la capacité à répondre aux audits ou aux exigences des détaillants.

3. Moyen-Orient et Eurasie : 2026 devient une fenêtre d'application plus forte

Le Moyen-Orient et l'Eurasie sont de plus en plus actifs en matière de réglementation des plastiques à usage unique. Historiquement, ces marchés étaient souvent considérés comme des marchés de services alimentaires axés sur les importations, avec une forte demande de gobelets et de couverts en plastique, de boîtes en mousse et d'emballages pour les plats à emporter. En 2026, cette image est en train de changer. Les Émirats arabes unis et la Géorgie sont deux exemples importants où la pression politique devient plus spécifique et où les restrictions au niveau des produits affectent les emballages des services alimentaires.

Pour les distributeurs d'emballages, les fournisseurs du secteur de l'hôtellerie et de la restauration et les chaînes de restaurants, cette situation crée une opportunité d'agir en amont. Les acheteurs qui se préparent avant que l'application ne devienne pleinement mature peuvent tester des alternatives, négocier un approvisionnement stable, revoir la conception des emballages de marque et éviter les pénuries soudaines lorsque les articles soumis à des restrictions sont retirés du marché.

Principaux marchés à surveiller au Moyen-Orient et en Eurasie

| Marché | 2026 Orientation politique | Principaux produits concernés | Opportunité d'affaires |

|---|---|---|---|

| Émirats arabes unis | Les restrictions s'étendent à d'autres produits de consommation en plastique à usage unique en 2026. | Gobelets, couvercles, assiettes, couverts, pailles, agitateurs et récipients alimentaires en polystyrène. | Emballages haut de gamme pour la restauration, destinés aux hôtels, aux cafés, aux traiteurs et aux chaînes de restaurants. |

| Géorgie | Les restrictions de 2026 concernent les produits en plastique à usage unique entrant en contact avec les aliments et les articles en polystyrène expansé. | Fourchettes, couteaux, cuillères, baguettes, assiettes, pailles, agitateurs, récipients en PSE, gobelets et couvercles en plastique. | Demande de remplacement direct pour la bagasse, le papier et les produits compostables destinés aux services alimentaires. |

| Arabie Saoudite | La réduction des déchets plastiques et le développement durable retiennent de plus en plus l'attention des gouvernements et des entreprises. | Les produits alimentaires jetables, les emballages de produits à emporter et les emballages de produits alimentaires vendus au détail doivent être surveillés. | Les circuits de l'hôtellerie, de la restauration rapide, des supermarchés et de la restauration collective à fort volume. |

| Qatar | Les secteurs de l'hôtellerie, de la restauration et de l'événementiel sont de plus en plus liés aux exigences de durabilité. | Boîtes repas, assiettes, gobelets, couverts et produits jetables pour la restauration événementielle. | Emballages haut de gamme pour les hôtels, les événements, les aéroports et la restauration d'entreprise. |

| Oman | Les politiques de réduction du plastique progressent graduellement, notamment en ce qui concerne les articles à usage unique. | Sacs en plastique, emballages pour la restauration et produits jetables pour la vente à emporter. | Croissance des distributeurs pour le papier, la bagasse et les produits de substitution compostables. |

| Bahreïn | La durabilité des emballages est de plus en plus importante pour les services alimentaires et les canaux d'importation. | Gobelets, pailles, assiettes en plastique et emballages des plats à emporter dans les restaurants. | Lignes de produits d'éco-emballage pour les entreprises de restauration. |

| Turquie | Les restrictions sur les sacs en plastique et les discussions sur la durabilité des emballages favorisent une transition progressive. | Gobelets en papier, boîtes alimentaires, sacs à emporter et emballages alimentaires durables. | Approvisionnement régional, emballage de marque pour les services alimentaires et distribution à l'exportation. |

Pourquoi les Émirats arabes unis et la Géorgie sont-ils importants en 2026 ?

Les EAU est importante parce que ses restrictions pour 2026 touchent directement les produits courants de la restauration tels que les gobelets en plastique, les couvercles, les assiettes, les couverts et les contenants alimentaires en polystyrène. Cet aspect est très important sur le plan commercial, car le pays dispose d'un vaste secteur de l'hôtellerie, d'un marché des restaurants haut de gamme, d'importantes activités de restauration et d'une forte culture des cafés. Les acheteurs de ce marché sont souvent attentifs à l'aspect de l'emballage, à la personnalisation de la marque et à la fiabilité des livraisons.

Géorgie est importante parce qu'il s'agit d'un cas clair pour 2026 où les produits en plastique entrant en contact avec les denrées alimentaires sont restreints. Le champ d'application des produits comprend des articles que les distributeurs de services alimentaires comprennent immédiatement : fourchettes, couteaux, cuillères, baguettes, assiettes, pailles, agitateurs, récipients alimentaires en polystyrène expansé, gobelets et couvercles. Cela crée une demande directe pour des lignes de produits alternatives, en particulier pour les importateurs qui doivent approvisionner les restaurants, les cafés, les supermarchés et les opérateurs de vente à emporter.

Note aux fournisseurs pour les acheteurs B2B

Pour des marchés tels que la Géorgie et les Émirats arabes unis, un portefeuille de produits complet est plus utile qu'une unité de stock isolée. Bioleader® peut aider les acheteurs à emballage alimentaire en papier, Les programmes de remplacement des services alimentaires comprennent des contenants en bagasse de canne à sucre, des gobelets en papier, des boîtes alimentaires en kraft et des couverts compostables.

Stratégie de produit recommandée pour cette région

Pour les restrictions concernant les gobelets en plastique

Les gobelets en papier, les gobelets à double paroi, les gobelets à paroi ondulée et les gobelets à revêtement à base d'eau conviennent aux cafés, aux hôtels et aux services de boissons à emporter. Les gobelets froids en PLA ne peuvent être envisagés que si les réglementations locales acceptent les plastiques compostables.

Pour le remplacement de la plaque et du bol en plastique

Les assiettes et les bols en bagasse sont pratiques pour les buffets, les événements, les repas à emporter et les aires de restauration. Ils offrent une alternative non plastique plus directe que les plastiques compostables dans les marchés plus stricts.

Pour le remplacement des boîtes à emporter en EPS

Les coquilles en bagasse et les boîtes alimentaires en papier kraft sont les remplaçants les plus directs des boîtes repas en mousse utilisées pour les plats à base de riz, les grillades, les hamburgers, les sandwiches et les plats cuisinés.

Pour les restrictions concernant les couverts en plastique

Les couverts en bois, les couverts en CPLA, les couverts en amidon de maïs et les kits de couverts emballés dans du papier peuvent être utilisés pour les repas à emporter, les services de restauration des compagnies aériennes, les services d'accueil et les programmes de livraison des restaurants.

Au Moyen-Orient, l'opportunité la plus forte n'est pas toujours le produit le moins cher. De nombreux acheteurs souhaitent des emballages propres, modernes et qui puissent être marqués, tout en soutenant les objectifs de développement durable. Les gobelets en papier imprimés sur mesure, les boîtes alimentaires en kraft, les assiettes en bagasse de qualité supérieure et les kits de couverts emballés sont donc particulièrement intéressants pour les hôtels, les cafés et les groupes de restauration.

4. Asie-Pacifique : De grands marchés, des vitesses politiques différentes

L'Asie-Pacifique est l'une des régions les plus importantes pour les emballages alimentaires jetables, mais aussi l'une des plus complexes. La région comprend de grandes économies manufacturières, des marchés urbains denses de livraison de nourriture, des destinations touristiques insulaires, des marchés développés très réglementés et des secteurs de la restauration à croissance rapide. Par conséquent, les règles relatives aux plastiques à usage unique n'évoluent pas à la même vitesse dans tous les pays.

Certains pays ont mis en place des restrictions générales qui incluent la vaisselle jetable. L'Inde a restreint une série d'articles en plastique à usage unique tels que les assiettes, les gobelets, les couverts, les pailles, les plateaux et les agitateurs. La Nouvelle-Zélande a interdit les assiettes, bols et couverts en plastique à usage unique, y compris les articles en plastique recyclable, biodégradable ou compostable. L'Australie utilise une approche basée sur l'État, de nombreux États limitant les couverts, les assiettes, les bols, les pailles et les articles de restauration en polystyrène expansé en plastique. La Chine continue de réduire les produits plastiques non dégradables à usage unique dans les services de restauration et les circuits de vente au détail. L'Asie du Sud-Est évolue plus progressivement, mais le tourisme, la pression exercée par les déchets urbains et la croissance des livraisons de nourriture accélèrent la demande de solutions de remplacement.

Paysage politique de l'Asie-Pacifique

| Marché | Orientations politiques | Opportunité d'emballage | Prudence stratégique |

|---|---|---|---|

| Chine | Les restrictions sur les produits plastiques non dégradables à usage unique se poursuivent dans la restauration et le commerce de détail. | Gobelets et bols en papier, récipients alimentaires en bagasse et alternatives biodégradables conformes. | Les politiques varient en fonction de l'application et de la région ; les déclarations relatives aux produits doivent être précises. |

| Inde | Les restrictions concernant les plastiques à usage unique portent sur les produits jetables en contact avec les aliments, tels que les assiettes, les gobelets, les couverts, les pailles et les plateaux. | Demande de grands volumes de papier à coût contrôlé, de fibres moulées et d'alternatives compostables. | La sensibilité au prix est élevée ; la performance du produit et l'efficacité du chargement sont importantes. |

| Japon | L'accent est mis sur la circulation des ressources en plastique, la réduction des déchets et l'utilisation responsable des emballages. | Emballages en papier de qualité supérieure, spécifications précises et solutions de remplacement sûres pour les aliments. | La documentation et la déclaration des matériaux sont essentielles. |

| Corée du Sud | La réduction du plastique est liée au recyclage, au tri des déchets et à la réduction de l'utilisation de produits jetables. | Contenants alimentaires en papier, gobelets et emballages durables vérifiés. | Il convient de vérifier les voies d'élimination locales et les attentes en matière d'étiquetage. |

| Thaïlande | La réduction des déchets plastiques reste importante, en particulier dans le commerce de détail, le tourisme et la restauration urbaine. | Gobelets en papier, boîtes en kraft, conteneurs en bagasse et emballages pour la restauration hôtelière. | Toutes les catégories de vaisselle à usage unique ne sont pas soumises aux mêmes restrictions. |

| Vietnam | La responsabilité en matière d'emballage et la gestion des déchets plastiques deviennent des thèmes politiques plus importants. | Bols en papier, boîtes en bagasse et alternatives aux plats à emporter pour les cafés et les marques de livraison. | L'élaboration de la politique est progressive ; l'éducation du marché est importante. |

| Malaisie | La réduction des plastiques progresse grâce à des politiques progressives et à des initiatives locales. | Les distributeurs de services alimentaires peuvent chercher des solutions de remplacement pour les emballages de produits à emporter et les gobelets pour boissons. | Vérifier la mise en œuvre au niveau de l'État et de la ville avant d'établir un devis. |

| Singapour | La réduction des déchets d'emballage et l'utilisation efficace des ressources sont les moteurs de pratiques durables dans le secteur de la restauration. | Bols en papier de qualité supérieure, récipients en bagasse et systèmes d'emballage compacts pour la vente à emporter en milieu urbain. | Les acheteurs apprécient la constance de la qualité, la clarté de la conception et la fiabilité de la logistique. |

| Indonésie | La réduction du plastique varie selon les villes et les régions, avec une forte pression dans les zones touristiques et côtières. | Emballages en bagasse, papier et kraft pour les restaurants, les hôtels et les chaînes de boissons. | Les règles locales et leur application varient d'une région à l'autre. |

| Philippines | Les gouvernements locaux et les politiques environnementales augmentent la pression sur les plastiques à usage unique. | Des alternatives écologiques pour les restaurants à service rapide, les cafés et les marchés touristiques insulaires. | Les attentes en matière de conformité peuvent varier d'une ville à l'autre et d'un acheteur à l'autre. |

| Australie | Les interdictions au niveau des États couvrent de nombreux articles en plastique à usage unique, notamment les couverts, les assiettes, les bols, les pailles et les récipients de service alimentaire en polystyrène expansé. | Bagasse, papier, carton et bois pour la distribution des services alimentaires. | Chaque État peut avoir des délais, des exemptions et des définitions de produits différents. |

| Nouvelle-Zélande | Les assiettes, bols et couverts en plastique sont interdits, y compris les versions en plastique recyclable, biodégradable et compostable. | Le carton, les fibres moulées, la bagasse et le bois sont des solutions plus fiables. | Ne pensez pas que le PLA ou le plastique compostable sont automatiquement acceptés. |

L'Asie-Pacifique exige un positionnement produit par produit

Une erreur fréquente consiste à décrire l'Asie-Pacifique comme un seul marché. Ce n'est pas exact. La demande de l'Inde, qui porte sur des volumes importants, est différente de celle de l'Europe. Les marchés publics japonais fondés sur la documentation. L'approche stricte de la Nouvelle-Zélande en matière de vaisselle en plastique diffère des restrictions progressives et municipales de l'Asie du Sud-Est. Le système australien, basé sur les États, nécessite un examen minutieux avant de faire des déclarations de conformité. Pour les exportateurs, la stratégie gagnante consiste à établir un positionnement flexible des produits en fonction de la destination, du matériau et de l'application.

Dans les marchés où les plastiques compostables sont acceptés, Gobelets en PLA peuvent être utilisés pour des boissons froides telles que le café glacé, les jus, les smoothies et les boissons événementielles. Toutefois, le PLA ne doit jamais être présenté comme un produit universellement exempt d'interdiction du plastique. Sur les marchés plus stricts, les gobelets en papier, les gobelets en fibre moulée, les bols en bagasse et les options en papier couché sans plastique peuvent constituer des choix plus sûrs.

Aperçu Bioleader® de l'Asie-Pacifique

La bonne question n'est pas “Quel est le matériau le plus écologique ?”. La question la plus pertinente pour l'acheteur est la suivante : “Quel matériau est accepté sur mon marché de destination, convient à mon type d'aliment, est étayé par des documents et est commercialement stable dans la quantité dont j'ai besoin ?”

Stratégie recommandée par type d'acheteur

Pour les importateurs de gros volumes

L'accent est mis sur les coquilles en bagasse, les gobelets et les bols en papier, les boîtes alimentaires en kraft et les couverts compostables. L'efficacité du chargement des conteneurs, la taille des cartons et la planification des emballages mixtes peuvent avoir une forte incidence sur le coût au débarquement.

Pour les cafés et les chaînes de restauration

Les gobelets en papier, les gobelets à parois ondulées, les gobelets pour boissons froides, les couvercles de gobelets et les manchons de marque sont essentiels. Le type de revêtement doit être choisi en fonction de la politique locale et des objectifs de durabilité du client.

Pour les hôtels et les marchés du tourisme

Les boîtes en kraft de qualité supérieure, les assiettes en bagasse, les bols en bagasse et les kits de couverts emballés peuvent être utilisés pour le service du petit-déjeuner, les événements, le service en chambre, les repas sur la plage et les plats à emporter.

Pour les marques de livraison et de préparation de repas

Les conteneurs en bagasse, les saladiers en papier, les bols à soupe en papier et les plateaux avec couvercle doivent être testés en termes d'étanchéité, d'empilabilité, de réchauffage, de résistance à l'huile et de mouvement d'acheminement.

En Asie-Pacifique, les fournisseurs les plus résistants sur le plan commercial n'imposeront pas un matériau pour chaque client. Ils aideront les acheteurs à choisir entre le papier, la bagasse, l'amidon de maïs, le CPLA, le bois et le PLA en fonction des règles du marché, de l'application alimentaire et du positionnement de l'acheteur. Ceci est particulièrement important pour les entreprises de livraison de nourriture et de vente à emporter, où la durabilité doit encore fonctionner sous une réelle pression opérationnelle.

5. Afrique : Le remplacement des boîtes à emporter en EPS est l'opportunité la plus pratique

L'Afrique mérite une attention particulière en 2026, car plusieurs pays vont au-delà du contrôle des sacs en plastique et adoptent des restrictions plus larges sur les plastiques à usage unique, les emballages alimentaires en mousse et les articles de restauration jetables. Toutefois, le marché africain ne doit pas être décrit de manière trop générale. L'opportunité commerciale la plus forte n'est pas nécessairement une interdiction de la vaisselle en plastique à l'échelle du continent. L'opportunité la plus pratique est le remplacement des boîtes à emporter en polystyrène expansé ou en polystyrène expansé.

Les conteneurs en mousse de polystyrène expansé sont largement utilisés sur de nombreux marchés africains de la restauration parce qu'ils sont bon marché, légers et familiers aux restaurants locaux. En même temps, ils sont difficiles à recycler, encombrants dans les flux de déchets et très visibles dans les rues et sur les côtes. Ils constituent donc une cible politique facile. Pour les fournisseurs d'emballages en fibre moulée et en papier, cela crée une demande directe de coquilles en bagasse, de plateaux en bagasse, de boîtes alimentaires en papier kraft et de bols en papier.

Carte des politiques et des opportunités pour l'Afrique

| Marché | Orientations politiques | Produits concernés | Alternatives les mieux adaptées |

|---|---|---|---|

| Seychelles | Restrictions précoces et strictes sur les ustensiles en plastique et les boîtes en polystyrène. | Fourchettes, cuillères, couteaux, assiettes, bols, tasses, plateaux et boîtes à emporter en polystyrène. | Assiettes en bagasse, coquilles en bagasse, gobelets en papier, bols en papier et couverts en bois. |

| Maurice | Les contrôles des produits plastiques à usage unique couvrent plusieurs articles de restauration. | Tasses, cuillères, fourchettes, couteaux, pailles, bols, plateaux, récipients à charnière, agitateurs et couvercles. | Conteneurs en bagasse, bols en papier, boîtes en kraft et kits de couverts emballés. |

| Rwanda | L'un des marchés africains où la réduction des plastiques est la plus forte, avec de larges restrictions sur les articles en plastique à usage unique. | Sacs en plastique, récipients alimentaires, couverts, pailles et autres plastiques à usage unique. | Emballages en fibre moulée, récipients alimentaires en papier et vaisselle non plastique. |

| Kenya | Une politique stricte en matière de sacs en plastique et des restrictions sur les plastiques à usage unique dans les zones protégées. | Bouteilles, gobelets, assiettes, couverts et pailles en plastique dans le contexte du tourisme et des zones protégées. | Emballages pour l'hôtellerie et le tourisme : assiettes en bagasse, gobelets en papier, boîtes en kraft et couverts en bois. |

| Ghana | L'interdiction nationale des produits en polystyrène expansé et en polystyrène expansé est annoncée pour 2027, ce qui fait de 2026 une année de préparation. | Emballages en polystyrène pour les plats à emporter, bols en mousse, gobelets en mousse et autres emballages alimentaires en polystyrène. | Coquilles en bagasse, plateaux en bagasse, boîtes alimentaires en papier et bols à soupe en papier. |

| Nigeria / Lagos | Un marché important avec des restrictions et des pressions croissantes sur les mousses et les plastiques à usage unique. | Contenants alimentaires en polystyrène, assiettes en plastique, couverts, pailles et emballages pour les plats à emporter. | Boîtes en bagasse à coût contrôlé, conteneurs en papier et lignes de vaisselle prêtes à l'emploi pour les distributeurs. |

| Sénégal | Les règles relatives à la gestion des produits et des déchets en plastique vont dans le sens d'une plus grande réduction. | Les plastiques des services de restauration, les récipients pour boissons et les articles d'emballage doivent être contrôlés. | Papier, bagasse et emballages alimentaires recyclables ou compostables. |

| Éthiopie | Les restrictions sur les sacs en plastique sont renforcées, avec des réformes plus larges de la gestion des déchets. | L'accent est actuellement mis sur les sacs en plastique, mais la pression exercée sur les emballages à usage unique pourrait s'accroître. | Étude de marché préliminaire pour les produits de remplacement du papier et des fibres moulées. |

| Tanzanie | Des restrictions sur les sacs de caisse en plastique sont mises en place ; la politique en matière de restauration est plus progressive. | L'accent est mis sur les sacs en plastique et sur la pression exercée par le tourisme et l'hôtellerie en matière de développement durable. | Emballages pour la restauration touristique, sacs en papier, assiettes en bagasse et récipients pour les plats à emporter. |

| Afrique du Sud | Les discussions sur la durabilité des emballages et les problèmes liés au plastique sont de plus en plus nombreuses. | Les emballages de restauration en PSE, les couverts en plastique et les emballages jetables doivent être contrôlés. | Emballages en papier prêts pour la vente au détail, conteneurs en fibre moulée et alternatives certifiées. |

| Zimbabwe | Les pressions politiques exercées par le passé visaient les contenants alimentaires en EPS/mousse. | Boîtes repas et emballages à emporter en mousse. | Coquilles en bagasse et boîtes à repas en papier kraft. |

Pourquoi l'Afrique est un marché important pour la bagasse

Pour les acheteurs africains de services alimentaires, le produit de remplacement doit être pratique. Il doit pouvoir contenir du riz chaud, des aliments frits, de la viande grillée, des sauces, des haricots, des ragoûts et des plats à emporter. Il doit également être suffisamment abordable pour les distributeurs et les vendeurs de produits alimentaires. C'est pourquoi l'emballage en bagasse de canne à sucre est commercialement pertinent. Elle offre une alternative à base de fibres aux contenants en mousse et peut être utilisée pour les boîtes à claire-voie, les plateaux, les bols et les assiettes.

Le programme de Bioleader contenants alimentaires en bagasse sont particulièrement pertinentes pour les marchés qui remplacent les boîtes repas en polystyrène. Pour les acheteurs du Ghana, du Nigeria, de l'île Maurice, des Seychelles et du Rwanda, le principal argument de vente n'est pas seulement la compostabilité. Il s'agit de la capacité à remplacer les emballages en mousse par une solution en fibre moulée sûre pour les aliments, adaptée aux micro-ondes, résistante à l'huile et prête pour l'exportation.

Bioleader® Aperçu de l'Afrique

L'opportunité africaine doit être décrite avec soin. Certains pays appliquent des interdictions nationales strictes. D'autres ont mis en place des contrôles régionaux, progressifs ou spécifiques à certains produits. Le message le plus précis et le plus utile d'un point de vue commercial est le suivant : “Le PSE et les emballages alimentaires en plastique à usage unique deviennent des cibles prioritaires, ce qui crée une demande d'alternatives pratiques non plastiques.”

Stratégie commerciale pour les distributeurs africains

Pour le Ghana et le Nigeria

Se concentrer sur le remplacement des boîtes à emporter en mousse. Construire une gamme de produits autour des coquilles en bagasse, des plateaux en bagasse, des boîtes alimentaires en papier kraft et des options de coutellerie à coût contrôlé.

Pour Maurice et les Seychelles

Produits de positionnement pour le tourisme, les hôtels, les restaurants, les cafés et la restauration. L'aspect haut de gamme et la documentation relative à la sécurité alimentaire sont plus importants qu'un simple prix bas.

Pour le Rwanda et le Kenya

Se concentrer sur les acheteurs sensibilisés à la politique, les canaux d'accueil et les distributeurs qui veulent des alternatives aux articles de restauration en plastique jetables.

Pour les marchés sensibles aux prix

Recommander des stratégies de conteneurs mixtes, des tailles standard, des UGS non personnalisés et un chargement efficace des cartons afin de réduire les coûts au débarquement.

L'opportunité de l'Afrique pour 2026 ne se résume pas à l'interdiction de tout plastique. Il s'agit d'une histoire de pressions politiques, de défis liés aux déchets urbains, de durabilité du tourisme et de remplacement progressif de la mousse et des articles de restauration en plastique. Pour les exportateurs, cela fait de l'Afrique une région importante pour les solutions d'emballage pratiques plutôt que pour les revendications de durabilité de premier ordre.

6. Amérique latine : Les contrôles progressifs des matières plastiques s'étendent aux emballages des services alimentaires

L'Amérique latine adopte un modèle de réduction progressive du plastique. De nombreux pays ont commencé par les sacs en plastique et les pailles, mais l'orientation politique est de plus en plus liée aux emballages des services alimentaires, aux ustensiles à usage unique, aux gobelets jetables, aux assiettes en plastique, aux conteneurs en polystyrène expansé et aux emballages de livraison. Pour les acheteurs B2B, cette région est importante car de nombreuses réglementations ne sont pas seulement des déclarations environnementales ; elles commencent à influencer les activités des restaurants, les emballages de vente au détail et la sélection des produits par les importateurs.

Le marché latino-américain est également diversifié sur le plan commercial. Certains acheteurs desservent des chaînes alimentaires haut de gamme et des supermarchés, tandis que d'autres approvisionnent des restaurants locaux de vente à emporter, des aires de restauration et des vendeurs de nourriture de rue. Cela signifie que la bonne solution doit trouver un équilibre entre la durabilité, le prix, la performance et la conformité locale.

Carte des politiques et des opportunités pour l'Amérique latine

| Marché | Orientations politiques | Articles à surveiller dans le secteur de la restauration | Opportunité d'emballage |

|---|---|---|---|

| Chili | La loi limite les produits à usage unique dans les établissements alimentaires et encourage les alternatives réutilisables, recyclables ou compostables. | Tasses, bols, couverts, assiettes, boîtes, plateaux, pailles, sachets et couvercles. | Emballages compostables certifiés en papier, bagasse et fibres moulées pour les services alimentaires. |

| Colombie | La loi 2232 prévoit l'élimination progressive de nombreux produits en plastique à usage unique par le biais d'une mise en œuvre graduelle. | Sacs en plastique, pailles, agitateurs, couverts, assiettes et autres catégories d'articles alimentaires au fil du temps. | Lignes de produits de remplacement précoce pour les distributeurs et les opérateurs de services alimentaires. |

| Pérou | La loi 30884 réglemente les plastiques à usage unique et les récipients jetables. | Sacs en plastique, pailles, emballages en mousse, vaisselle en plastique et récipients jetables. | Boîtes alimentaires en kraft, coquilles en bagasse, gobelets en papier et couverts compostables. |

| Mexique | Les restrictions concernant le plastique varient d'un État à l'autre et d'une ville à l'autre, la pression sur les articles à usage unique étant de plus en plus forte. | Sacs en plastique, pailles, récipients en mousse et produits jetables pour la restauration dans certaines régions. | Stratégies de produits spécifiques à chaque région pour les distributeurs et les détaillants de restaurants. |

| Costa Rica | L'orientation de la politique environnementale favorise la réduction des plastiques et les alternatives durables. | Les articles de restauration, les sacs et les emballages d'accueil en plastique doivent être contrôlés. | Solutions d'emballage pour le tourisme et l'éco-hospitalité. |

| Panama | Les mesures de réduction du plastique et les pressions en faveur du développement durable soutiennent la demande d'emballages alternatifs. | Pailles, sacs et produits jetables de restauration en plastique dans des contextes progressifs. | Gobelets en papier, assiettes en bagasse, boîtes alimentaires en kraft et kits de couverts. |

| Équateur | Les efforts locaux et nationaux de réduction du plastique soutiennent un positionnement plus large en matière de développement durable. | Les sacs en plastique, les emballages de restauration et les articles jetables doivent être surveillés. | Papier et fibres moulées pour les détaillants et les distributeurs de services alimentaires. |

| Argentine | Les règles relatives au plastique sont souvent élaborées dans le cadre de mesures prises au niveau des provinces ou des villes. | Sacs en plastique, pailles et certains articles de restauration en fonction du lieu. | L'éducation au marché et les portefeuilles d'emballages durables gérés par les distributeurs. |

| Brésil | Un marché important avec des initiatives de réduction du plastique au niveau des villes et des États. | Pailles, sacs, récipients en mousse et emballages de restauration en plastique dans certaines juridictions. | Gobelets en papier à grand volume, boîtes kraft, plateaux en fibre moulée et emballages alimentaires sur mesure. |

L'Amérique latine a besoin d'alternatives pratiques, et pas seulement de produits écologiques haut de gamme.

Les acheteurs d'Amérique latine ont souvent besoin d'emballages qui peuvent être compétitifs en termes de prix tout en soutenant les revendications en matière de développement durable. Un produit compostable haut de gamme peut être intéressant pour les restaurants ou les supermarchés haut de gamme, mais un distributeur desservant des milliers de petits restaurants peut avoir besoin de formats standard, d'un approvisionnement stable et d'un coût au débarquement compétitif. C'est là que la normalisation des produits prend toute son importance.

Par exemple, boîtes alimentaires en papier kraft peuvent servir des hamburgers, des nouilles, des plats à base de riz, des snacks, des aliments frits et des plats combinés à emporter. Ils sont faciles à marquer, efficaces pour les services alimentaires et familiers pour les clients. Les coquilles et les plateaux en bagasse peuvent ensuite couvrir les repas chauds et remplacer les boîtes en mousse. Ce portefeuille mixte offre aux importateurs une plus grande flexibilité que s'ils se contentaient d'un seul matériau.

Bioleader® Aperçu de l'Amérique latine

Dans les marchés à réglementation progressive, les acheteurs ne doivent pas attendre que tous les articles soumis à des restrictions soient pleinement appliqués. La stratégie la plus intelligente consiste à introduire rapidement d'autres UGS, à tester l'acceptation des clients et à établir des relations avec les fournisseurs avant que la demande n'augmente soudainement.

Gamme de produits recommandée pour l'Amérique latine

- Coquilles de bagasse : Le meilleur moyen de remplacer les boîtes de mousse, les repas chauds et les plats combinés à emporter.

- Boîtes alimentaires en papier : convient pour les hamburgers, les snacks, les nouilles, les repas à base de riz et les plats à emporter de marque.

- Gobelets en papier : utile pour le café, les boissons froides et la restauration événementielle.

- Bols à soupe et saladiers en papier : bien adapté à la livraison, à la préparation des repas et aux aires de restauration.

- Couverts compostables ou en bois : qui sont en mesure de limiter l'utilisation de fourchettes, couteaux et cuillères en plastique.

L'Amérique latine est une région où les importateurs doivent allier sensibilisation aux politiques et réalisme commercial. La stratégie d'emballage la plus performante comprendra généralement plusieurs catégories de matériaux plutôt qu'un seul produit “parfait”. Cela permet aux distributeurs de servir des restaurants à différents niveaux de prix tout en s'éloignant du plastique et de la mousse conventionnels.

7. Les pays insulaires et les marchés du tourisme : Petits pays, signaux forts d'interdiction du plastique

Les nations insulaires sont souvent parmi celles qui progressent le plus rapidement en matière de restriction des plastiques, car elles sont directement confrontées à la pollution marine par les plastiques. Les capacités de gestion des déchets peuvent être limitées, le tourisme est très visible et les plages sont au cœur de l'économie nationale. Pour ces pays, les pailles, les gobelets, les couverts, les assiettes et les boîtes en mousse à emporter en plastique ne sont pas seulement des problèmes de déchets ; ils affectent l'image du tourisme et les écosystèmes côtiers.

Ces marchés ne génèrent pas toujours les plus gros volumes de conteneurs, mais ils sont importants pour les services alimentaires de grande valeur, les hôtels, les centres de villégiature, les aéroports, les événements, la restauration de croisière et les marques d'écotourisme. Pour les exportateurs, les marchés insulaires peuvent également servir de preuve pour l'adoption d'emballages durables.

Marchés insulaires et touristiques à surveiller

| Marché | Signal politique | Éléments couramment touchés | Solutions Best-Fit |

|---|---|---|---|

| Maldives | L'élimination progressive des plastiques à usage unique est liée à la protection du milieu marin et au tourisme. | Pailles, gobelets, assiettes, couverts et autres articles à usage unique en plastique. | Gobelets en papier de qualité supérieure, assiettes en bagasse, boîtes en kraft et kits de couverts emballés. |

| Vanuatu | Connue pour ses restrictions strictes en matière de plastique parmi les nations insulaires du Pacifique. | Sacs en plastique, pailles, assiettes, couverts et récipients alimentaires en polystyrène. | Coquilles en bagasse, récipients alimentaires en papier et vaisselle non plastique. |

| Fidji | La réduction du plastique est liée au tourisme et à la protection du milieu marin. | Sacs en plastique, pailles, emballages pour les plats à emporter et produits jetables pour la restauration. | Lignes d'emballage pour hôtels et centres de villégiature utilisant du papier et des fibres moulées. |

| Samoa | Les efforts de réduction des plastiques dans les îles du Pacifique soutiennent les alternatives aux plastiques jetables. | Les sacs en plastique, les pailles et les emballages des services de restauration sont des domaines d'action privilégiés. | Gobelets en papier, assiettes en bagasse, bols et boîtes à emporter. |

| Jamaïque | Les restrictions élargies couvrent certains contenants alimentaires en plastique à usage unique, y compris les contenants en PE, PP et PLA. | Récipients alimentaires en plastique, récipients alimentaires en polystyrène expansé et articles connexes à usage unique. | Conteneurs en bagasse, boîtes alimentaires en papier et emballages alimentaires non plastiques. |

| Barbade | Les restrictions concernant le plastique jetable favorisent les alternatives non plastiques dans les services alimentaires. | Contenants, couverts et pailles en plastique à usage unique. | Vaisselle en bagasse, gobelets en papier et couverts en bois. |

| Bahamas | Les restrictions concernent plusieurs produits alimentaires en plastique et en polystyrène. | Gobelets, assiettes, récipients alimentaires, couverts en plastique et pailles en polystyrène. | Coquilles en bagasse, gobelets en papier et récipients alimentaires à base de fibres. |

| Belize | Les restrictions visent les emballages de restauration en plastique et en mousse. | Coquilles, assiettes, bols, tasses, couvercles, couverts et pailles en plastique. | Papier, bagasse et emballages compostables pour les services alimentaires. |

| Maurice | Marché insulaire axé sur le tourisme, avec contrôle des plastiques à usage unique. | Tasses, bols, plateaux, couverts, récipients à charnière et couvercles. | Bagasse de qualité supérieure, bols en papier, boîtes kraft et emballages pour hôtels. |

| Seychelles | Restrictions précoces et strictes sur les ustensiles en plastique et les boîtes en polystyrène. | Gobelets, assiettes, bols, plateaux, couverts et boîtes en polystyrène en plastique. | Assiettes en bagasse, coquilles, gobelets en papier et couverts en bois. |

Pourquoi les marchés insulaires sont-ils stratégiquement utiles ?

Les marchés insulaires sont souvent plus petits, mais leurs exigences en matière de développement durable sont très visibles. Les hôtels, les centres de villégiature et les opérateurs touristiques peuvent être plus enclins à adopter des emballages de qualité supérieure s'ils protègent l'image de la marque et s'alignent sur les engagements environnementaux. Les marchés insulaires se prêtent donc à l'utilisation de gobelets en papier personnalisés, de boîtes en kraft de marque, d'assiettes en bagasse de qualité supérieure et d'ensembles complets d'emballages pour la vente à emporter.

Le programme de Bioleader gobelets en papier et la vaisselle en fibre moulée peuvent aider les hôtels, les centres de villégiature, les sociétés de restauration et les chaînes de boissons qui souhaitent réduire l'exposition au plastique à usage unique sans compromettre la qualité du service. Pour ces acheteurs, l'emballage doit être à la fois fonctionnel et prêt à être présenté.

Aperçu du marché insulaire par Bioleader

Les nations insulaires montrent que la politique en matière de plastique n'est pas seulement une question de législation. Il s'agit aussi de pollution marine, de réputation touristique, de capacité de décharge limitée et d'attentes des clients. Pour les exportateurs, ces marchés exigent une qualité fiable, une conception propre et des revendications pratiques en matière de développement durable.

8. Amérique du Nord : Une réglementation mature mais fragmentée

L'Amérique du Nord est un marché mature pour l'emballage alimentaire durable, mais il ne s'agit pas d'un environnement réglementaire uniforme. Le Canada dispose d'un cadre fédéral plus centralisé pour certains articles en plastique à usage unique., tandis que le Les États-Unis sont fragmentés en États, Il faut donc tenir compte des règles de la ville et de la région. C'est pourquoi un acheteur américain peut être confronté à des exigences différentes selon que les produits sont vendus en Californie, à New York, à Washington, au New Jersey ou dans une autre juridiction.

Pour les exportateurs B2B, il s'agit d'éviter les simplifications excessives. Il n'existe pas aux États-Unis d'interdiction nationale de la vaisselle en plastique s'appliquant uniformément à tous les emballages des services alimentaires. Au lieu de cela, les acheteurs sont souvent confrontés à des interdictions au niveau des États, à des restrictions municipales sur les mousses, à des exigences des détaillants, à des règles relatives aux PFAS, à des normes d'approvisionnement et à des engagements de développement durable de la part des chaînes de restaurants ou des supermarchés.

Carte des politiques et des opportunités pour l'Amérique du Nord

| Marché | Orientations politiques | Impact de l'emballage des services alimentaires | Stratégie de l'acheteur |

|---|---|---|---|

| Canada | La réglementation fédérale sur les plastiques à usage unique limite les sacs de caisse, les couverts, certains articles de restauration, les porte-bagues, les bâtonnets et les pailles. | Les importateurs ont besoin d'alternatives aux couverts et articles de restauration en plastique problématiques. | Utiliser du papier certifié et bien documenté, des fibres moulées et des alternatives compostables. |

| États-Unis | Les réglementations fragmentées des États et des villes, ainsi que les exigences des détaillants et des chaînes de restauration. | Les interdictions de PSE, les règles sur les pailles, les lois sur les sacs en plastique, les restrictions sur les PFAS et les règles d'étiquetage sur la compostabilité varient d'un marché à l'autre. | Confirmer les règles de l'État de destination avant d'établir des devis ou de faire des déclarations de conformité. |

| Californie | L'un des environnements politiques les plus solides en matière d'emballage, de recyclage, d'étiquetage et de préoccupations liées aux PFAS. | Les acheteurs d'emballages pour les services alimentaires exigent souvent une documentation solide et des revendications précises. | Les fibres moulées sans PFAS, les emballages en papier et les produits compostables vérifiés sont acceptés. |

| New York | Restrictions sur les contenants alimentaires en mousse et pression plus large en faveur de la réduction du plastique. | Le remplacement de l'emballage des plats à emporter par du PSE reste d'actualité. | Coquilles en bagasse, plateaux en fibre moulée et récipients alimentaires en papier. |

| Washington | Une orientation politique forte en matière de durabilité des emballages et d'utilisation des PFAS. | Les emballages des services alimentaires doivent être examinés du point de vue de la sécurité des matériaux et des revendications environnementales. | Des produits sans PFAS et une documentation technique claire. |

| New Jersey | Les restrictions concernant les sacs à usage unique et les contenants en mousse influencent les choix d'emballage des services alimentaires. | Les contenants pour aliments à emporter et les produits jetables des services alimentaires sont soumis à des restrictions locales. | Papier, bagasse et alternatives à base de fibres avec documentation sur le contact alimentaire. |

Les acheteurs nord-américains regardent au-delà de l'interdiction elle-même

En Amérique du Nord, un acheteur peut poser des questions qui vont au-delà de l'autorisation légale d'un produit. Il peut demander si les emballages en fibre moulée sont exempts de PFAS, si les produits compostables sont acceptés dans les programmes de compostage locaux, si le produit peut être étiqueté comme compostable, s'il répond aux normes des détaillants et si les produits en fibre moulée d'origine chinoise sont exposés à des mesures correctives commerciales ou à des droits de douane supplémentaires.

L'Amérique du Nord est donc un marché à fort potentiel mais à fortes exigences. L'emballage doit être pratique, rentable, bien documenté et conforme aux règles d'étiquetage locales. Plateaux en bagasse avec couvercles, Les boîtes à claire-voie, les bols en papier et les couverts compostables sont autant d'options intéressantes, mais l'acheteur doit vérifier les règles de l'État de destination et la structure des coûts d'importation avant de passer de grosses commandes.

Bioleader® Insight d'Amérique du Nord

Sur le marché américain, la conformité n'est pas seulement environnementale. Il peut également s'agir de règles d'emballage spécifiques à un État, d'exigences en matière de PFAS, de règles d'étiquetage relatives à la compostabilité et d'exposition aux droits de douane. Les acheteurs doivent travailler avec leur courtier en douane local et leur conseiller juridique avant de prendre des décisions définitives en matière de réclamations ou d'importations.

9. Quels sont les matériaux les plus pratiques pour les acheteurs mondiaux ?

Aucun matériau ne peut à lui seul répondre à toutes les exigences du marché. La meilleure stratégie d'emballage global est une stratégie de portefeuille. Les acheteurs doivent sélectionner les matériaux en fonction de l'utilisation du produit, du marché de destination, de l'infrastructure d'élimination locale, du budget, des besoins de certification et des attentes des clients.

Comparaison des matériaux pour les marchés des restrictions en plastique en 2026

| Matériau | Meilleures applications | Points forts | Mise en garde concernant la conformité |

|---|---|---|---|

| Bagasse de canne à sucre | Coquilles, assiettes, bols, plateaux, récipients alimentaires. | Remplace avantageusement les récipients alimentaires en EPS et en plastique ; convient aux repas chauds et aux plats à emporter. | L'absence de PFAS et la documentation relative au contact avec les denrées alimentaires doivent être vérifiées. |

| Papier kraft et carton | Boîtes alimentaires, bols à soupe, saladiers, gobelets en papier et récipients à emporter. | Il s'agit d'un produit de marque, familier aux acheteurs de services alimentaires et adapté à de nombreux formats de vente à emporter. | Le type de revêtement a son importance ; les revêtements en PE, PLA et à base d'eau peuvent être traités différemment. |

| Papier couché sans plastique | Les gobelets en papier, les bols en papier et les récipients alimentaires recouverts d'un revêtement en plastique font l'objet d'un examen minutieux. | Un positionnement plus fort sur les marchés préoccupés par les emballages en plastique. | Les déclarations de performance, de recyclabilité et de certification doivent être étayées par des essais. |

| Bois | Couverts, agitateurs et petits ustensiles de restauration. | Simple, non plastique et largement accepté dans de nombreux marchés stricts. | L'expérience du client, le contrôle des échardes et la qualité du contact alimentaire doivent être vérifiés. |

| CPLA / amidon de maïs | Couverts, kits repas, ensembles d'ustensiles emballés et articles de restauration sélectionnés. | Utile là où les plastiques compostables sont acceptés et où le compostage industriel existe. | Peut encore être classé comme plastique dans certaines interdictions ; un examen du marché de destination est nécessaire. |

| PLA | Gobelets pour boissons froides, gobelets pour boissons transparentes, emballages pour salades et desserts dans les marchés acceptés. | Aspect clair et positionnement des matériaux d'origine végétale pour le service de boissons froides. | Ne convient pas pour les boissons chaudes ; n'est pas automatiquement exemptée des interdictions relatives au plastique. |

Pourquoi la bagasse est souvent le substitut le plus sûr à la mousse de polystyrène expansé

Les récipients alimentaires en mousse EPS constituent l'une des cibles politiques les plus courantes, car ils sont difficiles à recycler et très visibles dans les flux de déchets. Pour cette catégorie, la bagasse de canne à sucre est souvent le substitut le plus pratique. Elle est à base de fibres, convient à de nombreuses applications alimentaires chaudes et peut être moulée en coquilles, plateaux, bols et assiettes.

Les acheteurs qui évaluent le remplacement de la mousse peuvent également consulter la discussion de Bioleader® axée sur le terrain, Les boîtes à coquilles en bagasse de canne à sucre sont-elles fiables ?, qui se concentre sur des facteurs de performance pratiques tels que la résistance aux fuites, les mouvements de distribution, le réchauffage et la compatibilité alimentaire. Ces questions d'utilisation réelle sont exactement ce que les importateurs devraient tester avant de passer de la mousse à la fibre.

Orientation du produit Bioleader

Pour les acheteurs qui se préparent aux restrictions sur le plastique de 2026, Bioleader® recommande de construire un portefeuille de remplacement de base autour des coquilles en bagasse, des assiettes en bagasse, des gobelets en papier, des boîtes en papier kraft, des bols à soupe en papier, des bols à salade en papier et de la coutellerie compostable. Cette combinaison couvre la plupart des catégories réglementées de services alimentaires sans dépendre d'un seul matériau pour chaque application.

10. Que devraient faire les importateurs et les marques de produits alimentaires en 2026 ?

La décision la plus importante pour 2026 ne consiste pas simplement à choisir un produit “vert”. Les importateurs et les marques de produits alimentaires doivent créer une feuille de route pour les emballages prêts à être mis en conformité. Cette feuille de route doit identifier les produits actuels à risque, les matériaux acceptables dans chaque marché de destination, la documentation requise et les performances des produits alternatifs dans des conditions réelles de restauration.

Liste de contrôle pratique pour l'approvisionnement

- Confirmer le marché de destination : les règles relatives au plastique peuvent varier selon le pays, l'état, la ville ou la chaîne de restauration.

- Identifier la catégorie de produits à usage restreint : les couverts, les tasses, les assiettes, les bols, les pailles, les couvercles, les récipients en polystyrène expansé et les produits en papier couché peuvent être traités différemment.

- Vérifiez si les plastiques compostables sont acceptés : Le PLA et le CPLA peuvent être autorisés sur certains marchés, mais restreints sur d'autres.

- Demander la documentation du matériel : demander des informations sur la composition des matériaux, le type de revêtement, la sécurité au contact des aliments et la compostabilité, le cas échéant.

- Tester des applications alimentaires réelles : les soupes chaudes, les aliments gras, le curry, les aliments frits, les salades réfrigérées, les mouvements de livraison et le réchauffage au micro-ondes doivent être testés avant les commandes en gros.

- Examiner les exigences relatives aux PFAS : Les emballages alimentaires en fibre moulée doivent être vérifiés pour s'assurer qu'ils ne contiennent pas de PFAS lorsque les acheteurs ou les règles locales l'exigent.

- Calculer le coût au débarquement : le prix unitaire, le volume du carton, le chargement du conteneur, le fret, les droits de douane et les frais de manutention locaux sont autant d'éléments qui influent sur la compétitivité finale.

- Constituer un portefeuille de produits mixtes : combiner la bagasse, le papier, le kraft, le bois et les matériaux compostables au lieu de s'en tenir à un seul matériau.

Feuille de route recommandée pour les achats

| Étape | Action de l'acheteur | Pourquoi c'est important |

|---|---|---|

| Étape 1 | Cartographier les UGS actuelles pour le plastique et la mousse. | Permet d'identifier les produits les plus exposés au risque d'assurance. |

| Étape 2 | Sélectionner les matériaux de remplacement en fonction de l'application. | Évite l'erreur d'utiliser un matériau pour chaque type d'aliment. |

| Étape 3 | Demander des échantillons et des documents techniques. | Permet de tester les performances et de vérifier la conformité avant l'achat. |

| Étape 4 | Tester la compatibilité alimentaire et les performances de livraison. | Réduit les plaintes dues aux fuites, au ramollissement, à la déformation ou à la défaillance du couvercle. |

| Étape 5 | Confirmer les exigences locales en matière d'importation et d'étiquetage. | Évite les problèmes de conformité avec les douanes, les détaillants ou les marchés. |

| Étape 6 | Passez des commandes d'essai avant de procéder à une conversion à grande échelle. | Elle donne aux distributeurs le temps de recueillir les réactions des clients et d'ajuster la gamme de produits. |

Pour les marques et les distributeurs de produits alimentaires, l'approche la plus résiliente consiste à commencer par les catégories à haut risque : boîtes en mousse PSE, couverts en plastique, assiettes en plastique, gobelets en plastique, pailles en plastique et emballages à emporter enduits de plastique. Une fois ces catégories répertoriées, les acheteurs peuvent élaborer un plan de transition structuré en utilisant la bagasse, le papier, le kraft et des solutions de remplacement pour les couverts.

11. Solutions Bioleader® pour les marchés mondiaux de la restriction des plastiques

Bioleader® fournit des emballages jetables pour les services alimentaires aux acheteurs mondiaux qui se préparent aux restrictions sur le plastique, à l'interdiction des contenants en mousse et à la transition vers l'emballage durable. Le portefeuille de produits de l'entreprise couvre plusieurs voies de remplacement au lieu de s'appuyer sur un seul matériau. C'est important car les pays traitent différemment le plastique, les plastiques compostables, les revêtements en papier et les fibres moulées.

Pour les importateurs, les grossistes en emballages, les chaînes de restaurants, les fournisseurs de services de restauration et les marques de livraison de produits alimentaires, Bioleader® peut aider à la sélection des produits par application, y compris les repas chauds, les soupes, les salades, les boissons froides, les combinaisons à emporter, les plateaux de restauration, les ensembles de couverts et les emballages personnalisés.

Lignes de produits de base pour la demande politique de 2026

Conteneurs et coquilles en bagasse de canne à sucre

Convient pour remplacer les boîtes à emporter en mousse EPS, les conteneurs de repas en plastique et les plateaux jetables. Recommandé pour les restaurants, la livraison de nourriture, la préparation de repas, la restauration rapide et la restauration collective.

Assiettes, bols et plateaux en bagasse

Pratique pour la restauration, les hôtels, les buffets, les événements et la restauration rapide. Ces produits soutiennent les applications d'aliments chauds et les stratégies d'emballage en fibre moulée.

Gobelets et bols en papier

Convient pour le service de boissons, les soupes, les nouilles, les salades, les desserts et les plats à emporter. Les options d'enrobage doivent être sélectionnées en fonction des exigences du marché et de l'application alimentaire.

Boîtes alimentaires en papier kraft

Marquable et polyvalent pour les hamburgers, les repas à base de riz, les snacks, les aliments frits, les produits de boulangerie et les emballages de livraison.

Couverts compostables

Les kits de couverts CPLA, en amidon de maïs et emballés peuvent soutenir les marchés limitant les fourchettes, couteaux et cuillères en plastique et les accessoires de restauration.

Soutien à l'emballage personnalisé

Bioleader® prend en charge l'impression personnalisée, l'emballage sous marque de distributeur, la mise en correspondance des spécifications des produits et la planification de cartons prêts à l'exportation pour les acheteurs B2B.

Les acheteurs qui ont besoin d'une gamme complète de couverts de remplacement peuvent explorer la gamme de produits de Bioleader®. couverts biodégradables et compostables La gamme de produits de la marque "S" comprend des fourchettes, des cuillères, des couteaux et des sets emballés pour les plats à emporter, la restauration et la distribution de services alimentaires. Pour les acheteurs de soupes, de salades et de repas livrés, bols à soupe en papier avec couvercles et les saladiers en papier peuvent constituer des alternatives pratiques aux saladiers en plastique et aux récipients en mousse.

Besoin d'un portefeuille d'emballages prêt à être utilisé ?

Bioleader® peut aider les importateurs et les distributeurs à élaborer une stratégie de produits mixtes pour les marchés de restriction plastique 2026, y compris la vaisselle en bagasse de canne à sucre, les boîtes alimentaires en papier kraft, les gobelets en papier, les bols en papier et les couverts compostables. Pour obtenir un devis précis, les acheteurs doivent préparer le marché cible, le type de produit, la quantité, l'exigence de couvercle, l'exigence d'impression et les documents de certification préférés.

12. Perspectives finales : 2026 est l'année où il faut se préparer, et non attendre

L'orientation mondiale est claire : les emballages jetables des services alimentaires deviennent une catégorie réglementée. Les gouvernements ne ciblent pas seulement les sacs en plastique et les pailles ; ils s'intéressent de plus en plus aux couverts en plastique, aux gobelets, aux assiettes, aux bols, aux couvercles, aux récipients pour les repas à emporter et aux emballages en mousse EPS. Pour les acheteurs B2B, la meilleure réponse n'est pas d'attendre la date finale de mise en application. La meilleure réponse est de se préparer à l'avance, de tester des alternatives et de construire un portefeuille d'emballages capable de s'adapter aux différentes règles régionales.

La stratégie la plus fiable est la diversification des matériaux. La bagasse de canne à sucre remplace avantageusement la mousse et les contenants de repas en plastique. Le papier kraft et le carton sont efficaces pour les emballages de marques à emporter. Le papier couché sans plastique peut aider les marchés préoccupés par les revêtements en plastique. Les couverts en bois sont simples et largement acceptés. Les produits en CPLA, en amidon de maïs et en PLA peuvent être utiles là où les plastiques compostables sont légalement acceptés et soutenus par des systèmes d'élimination appropriés.

En 2026, l'emballage alimentaire durable n'est plus seulement un message marketing. Il fait désormais partie intégrante de la conformité réglementaire, de la protection de la marque et de la résilience de la chaîne d'approvisionnement. Les acheteurs qui agissent tôt peuvent réduire les risques, s'assurer des fournisseurs stables, tester correctement les produits et renforcer les revendications en matière de durabilité avant que le marché ne devienne plus encombré.

FAQ : Règlement 2026 sur la vaisselle en plastique et alternatives durables

1. Tous les pays interdiront-ils la vaisselle en plastique en 2026 ?

Les règles relatives à la vaisselle en plastique varient selon les pays, les États et les villes. Certains marchés limitent déjà les couverts, assiettes, gobelets et récipients en PSE en plastique, tandis que d'autres se concentrent encore sur les sacs en plastique ou sur la réduction progressive du plastique. Les acheteurs doivent vérifier le marché de destination avant d'importer.

2. Les gobelets en PLA sont-ils toujours autorisés dans le cadre des interdictions de plastique ?

Non. Le PLA est d'origine végétale et compostable dans des conditions industrielles appropriées, mais certaines réglementations le classent encore dans la catégorie des plastiques. Les gobelets en PLA ne doivent être utilisés que lorsque les réglementations locales acceptent les produits en plastique compostable et lorsque les applications de boissons froides sont adaptées.

3. Quel est le meilleur substitut aux boîtes à emporter en mousse EPS ?

Les coquilles en bagasse de canne à sucre et les conteneurs alimentaires en fibre moulée sont parmi les plus pratiques pour remplacer les boîtes à emporter en mousse EPS. Les boîtes alimentaires en papier kraft peuvent également convenir en fonction du type d'aliment, du niveau de sauce et des exigences de livraison.

4. Quels documents les importateurs doivent-ils demander pour la vaisselle écologique ?

Les importateurs doivent demander les spécifications des produits, les rapports d'essais de contact avec les aliments, les déclarations de matériaux, les certificats de compostabilité le cas échéant, les déclarations d'absence de PFAS pour les emballages en fibre moulée, les détails des cartons et tous les documents requis par le marché de destination.

5. Quelles sont les régions qui offrent les meilleures opportunités pour la vaisselle durable à l'horizon 2026 ?

Les régions à fort potentiel sont l'Europe, les Émirats arabes unis, la Géorgie, l'Inde, l'Australie, la Nouvelle-Zélande, le Ghana, le Nigeria, l'île Maurice, les Seychelles, le Chili, la Colombie, le Canada et les marchés touristiques insulaires. Les opportunités de produits diffèrent d'une région à l'autre, c'est pourquoi les acheteurs devraient constituer un portefeuille de matériaux mixtes.

6. La vaisselle en bagasse convient-elle pour les aliments chauds ?